unit root test in r package|phillips perron unit root test : wholesaling The problem with R is that there are several packages that can be used for unit root tests. Just to mention another one, > library (tseries) > adf.test (X,k=0) Augmented . Previous Raised by Wolves: Season 1 Featurette - Ridley Scott Gives A Glimpse into His World Raised by Wolves: Season 1 Featurette .

{plog:ftitle_list}

Resultado da ARTCLUB STORE. Livros infanto-juvenis. Rua da Assembleia, 100, 27 e 28 andar, Centro, Rio de Janeiro/RJ, CEP: 20011-904 - Compre Mude Seus .

ford 5.4 compression test

unit root test meaning

The problem with R is that there are several packages that can be used for unit root tests. Just to mention another one, > library (tseries) > adf.test (X,k=0) Augmented .The functions are: adfTest Augmented Dickey-Fuller test for unit roots, unitrootTest the same based on McKinnons's test statistics.I am running the following unit root test (Dickey-Fuller) on a time series using the ur.df() function in the urca package. The command is: summary(ur.df(d.Aus, type = "drift", 6))

unit root test interpretation

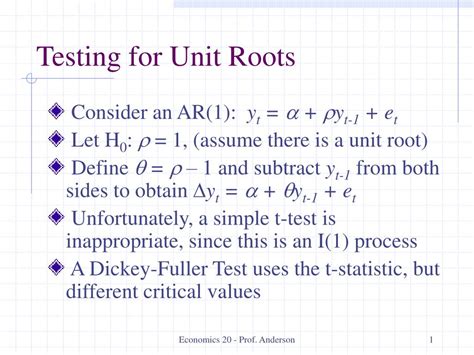

Unit root tests. Unit root tests help in assessing whether a time series is stationary. Due to the statistical issues that are associated with \(I\) (1) series, this is a very difficult task. Therefore, there is series of unit root tests .

Rstudio package urca developed by Bernhard Pfaff, Eric Zivot, Matthieu Stigler in 2016. “urca” is the abbreviation of the Unit Root and Cointegration Tests for Time Series Data. The package .A collection and description of functions for unit root testing. This is an interface to the unitroot tests implemented by B. Pfaff available through the R package urca which is required here. .

The idea of the DF-GLS test is to test for an autoregressive unit root in the detrended series, whereby GLS estimates of the deterministic components are used to obtain the detrended .Performs the Elliott, Rothenberg and Stock unit root test.

To perform a bootstrap version of the ADF unit root test on a single time series, use the boot_adf() function. The function allows to set many options, including the bootstrap method used (option bootstrap), the deterministic components included (option deterministics) and the type of detrending used (option detrend).While detrend = "OLS" gives the standard ADF test, detrend .Provides four addons for analyzing trends and unit roots in financial time series: (i) functions for the density and probability of the augmented Dickey-Fuller Test, (ii) functions for the density and probability of MacKinnon's unit root test statistics, (iii) reimplementations for the ADF and MacKinnon Test, and (iv) an 'urca' Unit Root Test Interface for Pfaff's unit root test suite.Performs the Augmented Dickey-Fuller test for the null hypothesis of a unit root of a univarate time series x (equivalently, x is a non-stationary time series). Rdocumentation. powered by. Learn R Programming . # ADF test for AR(1) process x <- arima.sim(list (order = c (1, 0, 0),ar = 0.2),n = 100) adf.test(x) .I am running the following unit root test (Dickey-Fuller) on a time series using the ur.df() function in the urca package. . You may want to pick a time series (maybe one already available in R or in a package) run the dickey fuller test on it and then use your function just for interested people to see what it does. $\endgroup .

2 uroot-package Index 16 uroot-package Unit Root Tests for Seasonal Time Series Description Canova and Hansen (CH) test for seasonal stability and Hylleberg, Engle, Granger and Yoo (HEGY) test for seasonal unit roots. Details Version >= 2.0.0 is a revival of the former package uroot. Some of the functions provided in theSeasonal unit roots and seasonal stability tests. P-values based on response surface regressions are available for both tests. P-values based on bootstrap are available for seasonal unit root tests.purtest implements several testing procedures that have been proposed to test unit root hypotheses with panel data. Unit root tests help in assessing whether a time series is stationary. Due to the statistical issues that are associated with \(I\) (1) series, this is a very difficult task. Therefore, there is series of unit root tests and proposals under which circumstances a test is more useful than another. . The tseries package contains the unit root .

Phillips-Perron Test Description. Performs the Phillips-Perron test for the null hypothesis of a unit root of a univariate time series x (equivalently, x is a non-stationary time series). Usage pp.test(x, type = c("Z_rho", "Z_tau"), lag.short = TRUE, output = TRUE) Arguments y: Vector to be tested for a unit root. type: Test type, either "none", "drift" or "trend".. lags: Number of lags for endogenous variable to be included. selectlags: Lag selection can be achieved according to the Akaike "AIC" or the Bayes "BIC" information criteria. The maximum number of lags considered is set by lags.The default is to use a "fixed" lag length set . rdrr.io Find an R package R language docs Run R in your browser. NonlinearTSA Nonlinear Time Series Analysis. Package index. Search the NonlinearTSA package . nonlinear unit root test. In NonlinearTSA: Nonlinear Time Series Analysis. Description Usage Arguments Value References Examples. View source: R/KSS_Unit_Root.R. Description. This .tailed unit root tests, such as the Augmented Dickey Fuller (ADF), to the entire sample of available data. Although widely employed, standard unit root tests have extremely low . In this paper, we introduce the R package exuber that deals with the detection of periods of mildly explosive dynamics (exuberance) in time series processes using .

Eviews 5 allows you to test the panel unit roots for the unbalanced data that is not possible with R and Stata.For example, even though Im–Pesaran–Shin and Fisher-type tests can be applied for unbalanced panel in Stata, it is not possible if we have some observations , with the gap i.e. we have data of country i for year 2002 and 2004 but not 2003 (assuming the lag to be greater .

If \(a = 1\), the model is nonstationary, where \(a\) is a stationary test. Unit Root Tests: Unit root tests are tests for stationarity in a time series. The shape of stationarity is if a shift in time doesn’t cause a change in the shape of the distribution. Unit roots are one cause for non-stationarity.The DF-GLS Test for a Unit Root. The DF-GLS test for a unit root has been developed by Elliott, Rothenberg, and Stock and has higher power than the ADF test when the autoregressive root is large but less than one. That is, the DF-GLS has a higher probability of rejecting the false null of a stochastic trend when the sample data stems from a time series that is close to being .

Unit root tests form an essential part of any time series analysis. We provide practitioners with a single, unified framework for comprehensive and reliable unit root testing in the R package bootUR.Unit root tests for stationarity have relevancy in almost every practical time series analysis. Deciding on which unit root test to use is a topic of active interest. . Summary This paper presents the R package CADFtest that allows unit root testing using the CovariateAugmented Dickey Fuller (CADF) test advocated in Hansen (1995). Differently . Details. All these tests except "hadri" are based on the estimation of augmented Dickey-Fuller (ADF) regressions for each time series. A statistic is then computed using the t-statistics associated with the lagged variable. The Hadri residual-based LM statistic is the cross-sectional average of the individual KPSS statistics .This paper introduces the R package exuber for testingstamping andperiods date -of mildly explosive dynamics (exuberanc e) in time series . The package computes test statis- . unit root tests have extremely low power in detecting episodes of explosive dynamics when these are interrupted by market crashes (Evans1991).

Test for a unit root, comparable to 'unitroot' from S-PLUS Finmetrics used in the examples on pp. 70-72 of Tsay (2005). NOTE: This help page is written without access to S-PLUS Finmetrics, and functionality beyond that in those two examples could change in the future. This work provides practitioners with a single, unified framework for comprehensive and reliable unit root testing in the R package bootUR, which addresses the needs of both novice users and expert users by giving full user-control to adjust the tests to one's desired settings. Unit root tests form an essential part of any time series analysis. We provide .

phillips perron unit root test

rdrr.io Find an R package R language docs Run R in your browser. tseries Time Series Analysis and Computational Finance. Package index. Search the tseries package. Functions. 188. . Phillips–Perron Unit Root Test Description. Computes the Phillips-Perron test for the null hypothesis that x has a unit root. Usage pp.test(x, alternative = c .

phillips perron test in r

statistic The value of the test statistic of the unit root test; p.value The p-value of the unit root test; details A list containing the detailed outcomes of the performed test, such as selected lags, individual estimates and p-values. specifications The specifications used in the test. Errors and warnings Error: Multiple time series not allowed.The null hypothesis of the ADF test is the presence of a unit root. The lag order to calculate the statistic of the ADF test is automatically selected according to the precedure by Ng \& Perron (2001). The null hypothesis of the KPSS test is stationarity. The statistic of the KPSS test is calculated at the lag order 4*(n/100)^0.25.pdR-package Panel Data Regression: Threshold Model and Unit Root Tests Description Functions for analysis of panel data, including the panel threshold model of Hansen (1999,JE), panel unit root test of Chang(2002,JE) based upon instuments generating functions (IGF), and panel seasonal unit root test based upon Hylleberg et al.(1990,JE). Details

In this paper we o er a brief survey of panel unit root testing with R. In fact, only two R packages, namely plm (Croissant and Millo2008) and punitroots (Kleiber and Lupi2011), implement panel unit root tests. In particular, seven panel unit root tests are implemented (three in plm and four in punitroots), plus one stationarity test (in plm).

ford 5.4 compression tester

Kapetanios, Shin and Snell(2003) nonlinear unit root test function Description. This function allows you to make Kapetanios, Shin and Snell(2003) nonlinear unit root test Usage KSS_Unit_Root(x, case, lags, lsm) Arguments

ford 5.4 compression tester adapter

Micro Macro Mundo Inc. 14900 S.W. 136th Street #103 Miami Florida 33196 U.S.A. PH: 786-250-3108 . Store Hours. 11 to 6 Weekdays 10 to 3 Saturdays Sundays CLOSED. Our products. Home » Manufacturers » Roco . Micro Macro Mundo Inc. Founded in 1986 in Miami Florida U.S.A. presents:

unit root test in r package|phillips perron unit root test